Your Guide to Medicare Premiums

Understanding what you can expect to pay in Medicare premiums can help you prepare for your health care expenses.

Different parts of Medicare come with different premiums—some are optional, some are required, and some can change based on your income level. We’ve created this guide to give you clarity on monthly Medicare premiums.

Before we dive into premiums, let’s review some terminology. The first thing to know is that Medicare is divided into four parts:

Most individuals qualify for Part A and Part B upon turning 65, so long as they or their spouse worked at least 10 years and paid into Social Security taxes. Parts A and B are considered “Original Medicare.”

Part C (also called Medicare Advantage) combines Parts A, B, and typically D into one plan. Medicare Part D covers prescription drugs. Parts C and D are additional coverage that you can purchase to bolster Original Medicare. While Medicare Parts A and B are mandated by federal and state governments, private insurance companies offer Part C and Part D plans.

Each of Medicare’s parts can come with premiums, or monthly payments, which may be conditional or mandatory.

Note: All figures listed here are based on 2024 data.

Original Medicare: Part A and Part B

Medicare Part A covers inpatient care: hospitalizations, skilled nursing care, hospice, and home health care. Medicare Part A is premium-free—for most people. If you or your spouse have worked at least 10 years (40 quarters) by the time you turn 65, you receive Medicare Part A at no monthly cost. However, if you or your spouse have worked less than 10 years, you can purchase Part A with a premium of up to $505 each month.

While most people may not pay a monthly premium for Medicare Part A, it is not free. You still pay out-of-pocket costs for medical services.

Enrollment penalties can also increase your monthly Part A costs. If you don’t purchase Medicare Part A when you are first eligible, your monthly premium can go up 10 percent. This applies for twice the number of years you could have had Part A but didn’t enroll. For example, if you didn’t sign up for Medicare Part A for two years after you were eligible, your premium would be 10 percent higher for four years. Then, the premium would go back down to your standard monthly rate.

Learn more about late enrollment penalties here.

Medicare Part B covers outpatient and preventive care—such as ambulance services, health screenings, and medical equipment. Unlike Part A, every Medicare beneficiary pays a monthly premium for Part B, with the exception of those who are eligible for full Medicaid, as Medicaid may cover their Part B premium.

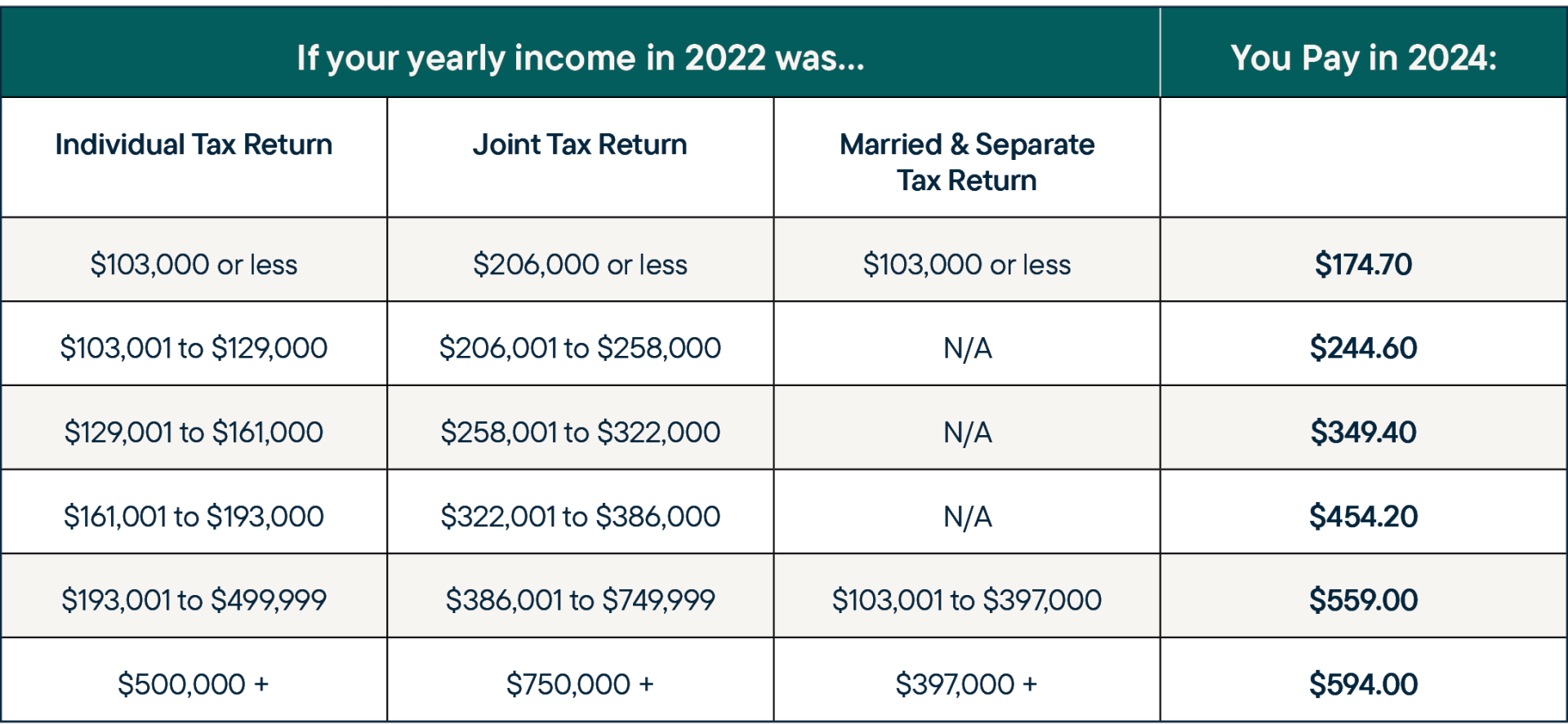

The cost of your Medicare Part B premium is based on your annual income from two years prior and how you file your tax return. The table below breaks down the Medicare Part B premiums for 2024.

It's important to know that even if you and your spouse file a joint tax return, you each pay an individual Part B monthly premium, as all Medicare parts and plans are individual coverage. If you have a qualifying life event, such as an end to or reduction in your employment, you may be able to submit an appeal to reduce your income surcharge.

Late enrollment penalties can also apply to Medicare Part B. If you wait too long to sign up for Medicare Part B, you can incur a 10 percent premium increase for each 12-month period you were eligible but did not enroll. For example, if you wait until 27 months after your eligibility ends, that totals two 12-month periods without coverage. As a result, your monthly premium would increase by 20 percent (10 percent per period x two 12-month periods) for the duration of your Part B coverage.

Additional Coverage: Medicare Part C and Part D

Medicare Part C, also known as Medicare Advantage, is available to purchase on top of Original Medicare. Medicare Advantage plans combine Parts A and B, and they often include prescription drug coverage (Part D) and cover additional services not included in Original Medicare. In many instances, Medicare beneficiaries pay no monthly premium for Part C.

However, it all depends on the insurance carrier and the benefits you choose. Your Medicare Advantage plan may come with a low monthly premium. It may cover some of the cost of your Part B monthly premium as an added benefit. Reach out to us for help assessing all your plan options. We’ll keep your current health care expenses in mind as we research available coverage.

You can also purchase prescription drug coverage in addition to Original Medicare. Standalone Part D plans have a monthly premium. You can save on this monthly premium, however, when you purchase a Medicare Part C plan which includes Part D coverage.

FAQS: Medicare Premiums

Does Medicare Part A have a monthly premium?

Usually not. It depends on your work history. But if you or your spouse have paid into Social Security taxes for at least 10 years, your Medicare Part A premium is waived.

Does Medicare Part B have a monthly premium?

Yes. For most people, it’s $174.70, but it can be more based on your income. See the chart above.

What if my income changes? Will it change my Part B monthly premium?

Your premium likely won’t change unless your income increases or decreases dramatically. It also may not change right away. Your Part B premium is calculated based on your taxable income from two years prior—for example, your 2024 rates are calculated based on your 2022 income.

Does Medicare Part C (Medicare Advantage) have a monthly premium?

Possibly, depending on the plan you choose. Many plans are available that have low or $0 monthly premiums.

Does Medicare Part D have a monthly premium?

Possibly, depending on the plan you choose. Standalone Part D plans have a monthly premium. You may bypass paying a separate Part D premium if your Part C plan includes prescription drug coverage.

What is the premium for a Medicare Supplement plan?

Medicare Supplement (Medigap) premium rates vary by the insurance carrier. Rates are determined by your age, gender, where you live, and when you enroll.

Want to learn more about Medicare premiums?

Whether you have questions about monthly premiums or choosing the right Medicare plan, we’re here for you! Contact an advisor at 937.915.3563 or schedule a call.

Already a RetireMed client? If you would like information about your Medicare plan premiums or have any other questions about your plan, call 877.222.1942 or schedule a call with a client advisor.

Share this article: